Building a Better Financial Product Marketplace

2025 ANNUAL REPORT

Building a Better Financial Product Marketplace

2025 ANNUAL REPORT

Better financial products depend on trustworthy, inclusive institutions. As workers across the country face growing debt and financial strain, Neighborhood Trust is helping thousands move away from extractive products—and into a system that prioritizes their financial well-being by using innovative approaches that center trust and equity without sacrificing commercial viability. Our approach is grounded in decades of experience and an unwavering commitment to helping workers achieve freedom from debt.

Better financial products depend on trustworthy, inclusive institutions. As workers across the country face growing debt and financial strain, Neighborhood Trust is helping thousands move away from extractive products—and into a system that prioritizes their financial well-being by using innovative approaches that center trust and equity without sacrificing commercial viability. Our approach is grounded in decades of experience and an unwavering commitment to helping workers achieve freedom from debt.

Letter from the CEO

Dear Friends and Colleagues,

It’s been nearly thirty years since Neighborhood Trust opened its doors as a nonprofit built to support the first CDFI credit union in Manhattan’s Washington Heights neighborhood. As we approach this remarkable milestone, I’ve been reflecting on how our roots in the credit union movement inform our vision for a more mainstream and accessible financial product marketplace that centers and empowers workers.

CDFI credit unions are guided by local member-owners rather than nameless shareholders, and they are driven by community impact, rather than profit-maximization. We know from decades of experience that these traits, paired with high-touch personal service, are what lead to life-changing improvements in a worker’s financial stability. Our challenge, however, has always been matching the vast needs of millions of low-income workers with resource-limited, mission-driven institutions like CDFI credit unions.

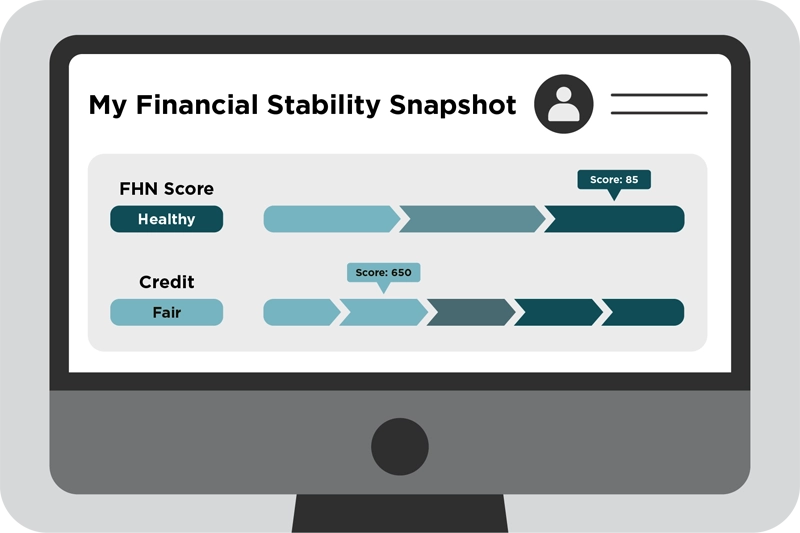

Then came 2025—a year like few others in history in terms of technological advancement. The proliferation of AI has created new promise and thrilling momentum for Neighborhood Trust’s work standing up a better, safer, and more accessible financial product marketplace. Technology is making it possible for CDFI credit unions to overcome historic barriers to scale, and for us to provide more holistic and transparent pathways out of debt for our clients. For example, we launched our Financial Snapshot tool, a visual dashboard that tracks financial vital signs and will soon offer dynamic product recommendations. We’re also enhancing the products we offer to our credit union customers, which in turn will help them accelerate scale and automate repetitive tasks while maintaining the human touch core to their DNA.

2025 also brought intensifying financial challenges for many clients, an increasingly uncertain political landscape, and widespread growth of exploitative financial services. These challenges only fueled our resolve to help workers achieve freedom from debt, to deliver results for clients, to innovate, and to deepen our connections with mission-aligned partners.

Select highlights:

- Our Financial Coaches served more than 8,000 workers, helping them navigate uncertainty and exploitation, and instead access and enroll in better, safer products from credit unions and CDFIs.

- We partnered with nearly 90 customers to bring our financial coaching to their networks, and launched a special campaign to serve the financial needs of essential workers at our fellow nonprofits.

- We welcomed new leadership and Board Members who bring expertise and networks that will significantly contribute to our effectiveness and ambitions.

- We fully embraced new applications of data and AI, launching pilots and proof-of-concepts that set us up to serve workers at massive scale in the coming years.

All of this hard work has paved the way for what we know will be a momentous 2026, in which we make significant progress to eradicate predatory financial services and build a better financial product marketplace for all workers. I hope you’ll read on to learn more about these accomplishments and the partnerships that made them possible in the pages ahead.

Thank you to our supporters, partners, and customers for partnering with us on this vision, and being part of our mission to support low-wage workers.

In partnership,

![]()

Justine, CEO

Letter from the CEO

Dear Friends and Colleagues,

It’s been nearly thirty years since Neighborhood Trust opened its doors as a nonprofit built to support the first CDFI credit union in Manhattan’s Washington Heights neighborhood. As we approach this remarkable milestone, I’ve been reflecting on how our roots in the credit union movement inform our vision for a more mainstream and accessible financial product marketplace that centers and empowers workers.

CDFI credit unions are guided by local member-owners rather than nameless shareholders, and they are driven by community impact, rather than profit-maximization. We know from decades of experience that these traits, paired with high-touch personal service, are what lead to life-changing improvements in a worker’s financial stability. Our challenge, however, has always been matching the vast needs of millions of low-income workers with resource-limited, mission-driven institutions like CDFI credit unions.

Then came 2025—a year like few others in history in terms of technological advancement. The proliferation of AI has created new promise and thrilling momentum for Neighborhood Trust’s work standing up a better, safer, and more accessible financial product marketplace. Technology is making it possible for CDFI credit unions to overcome historic barriers to scale, and for us to provide more holistic and transparent pathways out of debt for our clients. For example, we launched our Financial Snapshot tool, a visual dashboard that tracks financial vital signs and will soon offer dynamic product recommendations. We’re also enhancing the products we offer to our credit union customers, which in turn will help them accelerate scale and automate repetitive tasks while maintaining the human touch core to their DNA.

2025 also brought intensifying financial challenges for many clients, an increasingly uncertain political landscape, and widespread growth of exploitative financial services. These challenges only fueled our resolve to help workers achieve freedom from debt, to deliver results for clients, to innovate, and to deepen our connections with mission-aligned partners.

Select highlights:

- Our Financial Coaches served more than 8,000 workers, helping them navigate uncertainty and exploitation, and instead access and enroll in better, safer products from credit unions and CDFIs.

- We partnered with nearly 90 customers to bring our financial coaching to their networks, and launched a special campaign to serve the financial needs of essential workers at our fellow nonprofits.

- We welcomed new leadership and Board Members who bring expertise and networks that will significantly contribute to our effectiveness and ambitions.

- We fully embraced new applications of data and AI, launching pilots and proof-of-concepts that set us up to serve workers at massive scale in the coming years.

All of this hard work has paved the way for what we know will be a momentous 2026, in which we make significant progress to eradicate predatory financial services and build a better financial product marketplace for all workers. I hope you’ll read on to learn more about these accomplishments and the partnerships that made them possible in the pages ahead.

Thank you to our supporters, partners, and customers for partnering with us on this vision, and being part of our mission to support low-wage workers.

In partnership,

![]()

Justine, CEO

About the Workers We Served in 2025

Understanding our clients’ financial realities is essential to expanding access to good financial products. Their debt burdens, credit profiles, and reliance on predatory products inform our financial coaching priorities, product and partnership choices, and roadmap for eliminating debt.

Who Our Clients Are

Total clients served across all programs: 8,448

Total clients served across all programs: 8,448

TrustPlus: 2,228

Pathways: 4,898

NYC Financial Empowerment Centers: 1,322

Median annual income: $38,760

Women

People of color

Have at least one dependent

Their financial starting point

Debt burdens

Debt burdens

81% carry credit card debt at a median of $2,933

49% have personal loans at a median of $2,976

46% have collections with a median balance of $1,620

26% spend over 20% of their income on debt

Credit score

Credit score

53% have unestablished or subprime credit:

8% unestablished / 31% deep subprime / 14% subprime

Vulnerability to exploitation

Vulnerability to exploitation

51% have at least one predatory financial product on their credit report,

with a median balance of $2,473

Financial outlook*

Financial outlook*

81% are just getting by financially

52% rarely or never have money leftover at the end of the month

*TrustPlus clients only; based on survey responses

About the Workers We Served in 2025

Understanding our clients’ financial realities is essential to expanding access to good financial products. Their debt burdens, credit profiles, and reliance on predatory products inform our financial coaching priorities, product and partnership choices, and roadmap for eliminating debt.

Who Our Clients Are

Total clients served across all programs: 8,448

TrustPlus: 2,228

Pathways: 4,898

NYC Financial Empowerment Centers: 1,322

Median annual income: $38,760

Women

People of color

Have at least one dependent

Their financial starting point

Debt burdens

81% carry credit card debt at a median of $2,933

49% have personal loans at a median of $2,976

46% have collections with a median balance of $1,620

26% spend over 20% of their income on debt

Credit score

53% have unestablished or subprime credit:

8% unestablished / 31% deep subprime / 14% subprime

Vulnerability to exploitation

51% have at least one predatory financial product on their credit report,

with a median balance of $2,473

Financial outlook*

81% are just getting by financially

52% rarely or never have money leftover at the end of the month

*TrustPlus clients only; based on survey responses

Why We’re Building a Better System

Low-wage workers face a persistent and escalating affordability crisis. One in four adults are food insecure; nearly 40% have delayed or foregone healthcare because of cost; and over five million are in default on their student loans following the elimination of some relief and repayment programs.

Compounding these challenges are the defunding of healthcare subsidies, devastating cuts to SNAP, and an economy with a challenging job market. We have also been seeing an alarming trend of more clients being taken to collections and sued by creditors.

For workers who have been struggling for years, these worsening conditions are set to leave them with less cash, more stress, and sinking deeper into the vicious cycle of debt.

Predatory institutions are thriving in this environment. Payday loans, high-interest credit cards, and subprime auto loans use aggressive marketing and promise quick relief—preying on people desperate for options and a reprieve from not having enough to make ends meet. With federal oversight and regulations weakened or eliminated, these institutions will continue to proliferate. As we detailed in our 2024 Annual Report, this exploitative system is designed to extract wealth from those who can least afford it.

But safe, affordable alternatives to high-cost predatory debt do exist. CDFI credit unions and mission-aligned financial institutions are structured to serve, and not exploit, low-income communities. These institutions are the foundation of the inclusive system Neighborhood Trust is helping to strengthen.

By connecting more workers to better products and institutions, we are taking clients away from the predatory marketplace and fueling the growth of a safer, worker-centered system. At the same time, the data and insights we gather about how these better products affect cash flow and debt inform how these institutions can better serve workers.

Impact in Action

Data from our team of Financial Coaches in 2025 indicates that our approach is gaining traction and meaningfully impacting client trajectories out of debt. To measure progress out of debt, we use a framework with five indicators that signal greater financial security:

![]()

Reduced debt and predatory financial services

Lowering debt balances and using fewer high-cost, exploitative products

![]()

Healthy credit profiles

Achieving a near-prime or prime score

![]()

Access to helpful financial solutions

Being in a better position to be approved for safe, affordable financial products

![]()

Improved cash flow

Increasing cash flow, allowing for savings and investment in bigger financial goals

![]()

Increased financial self-efficacy and power*

Successfully meeting personal financial goals and feeling growing financial confidence and power that builds over time

*“How Executive Functioning and Financial Self-efficacy Predict Subjective Financial Well-Being via Positive Financial Behaviors,” Journal of Family and Economic Issues (2022)

2025 Impact Statistics

HERE’S HOW THESE INDICATORS SHOWED UP IN OUR 2025 CLIENT PORTFOLIO.

Reductions in debt and predatory financial services

Reductions in debt and predatory financial services

Lower debt balances among clients with the following types of debt at intake

51% reduced personal loans by a median of $1,428

47% reduced credit card debt by a median of $1,345

65% reduced auto loan debt by a median of $4,228

58% reduced collections debt by a median of $1,068;

29% eliminated their collections entirely

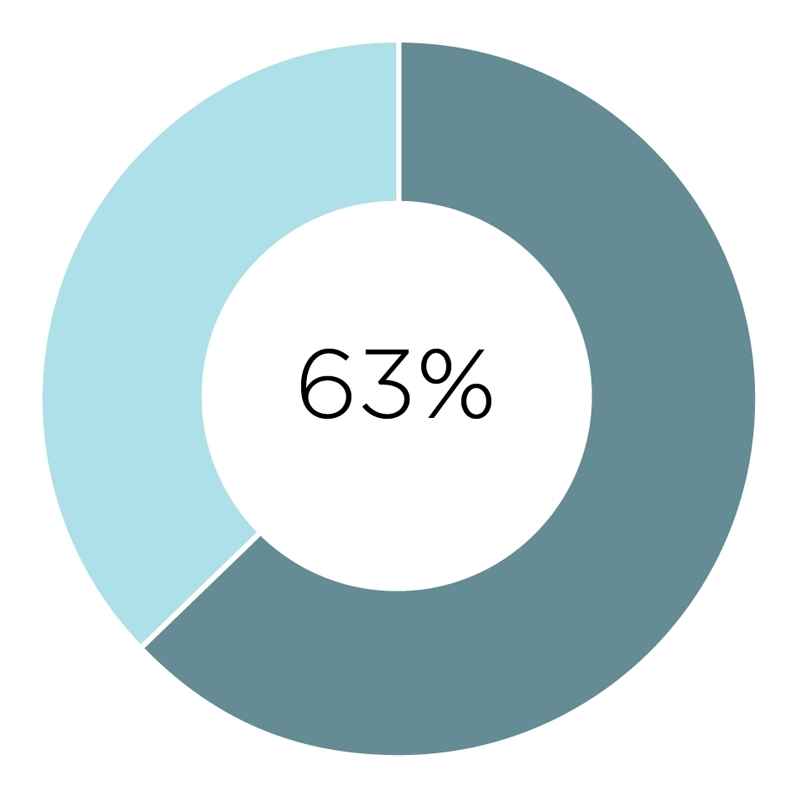

63% reduced instances of predatory debt;

28% entirely eliminated predatory debt from their credit reports

Improvements to credit scores and profiles

Improvements to credit scores and profiles

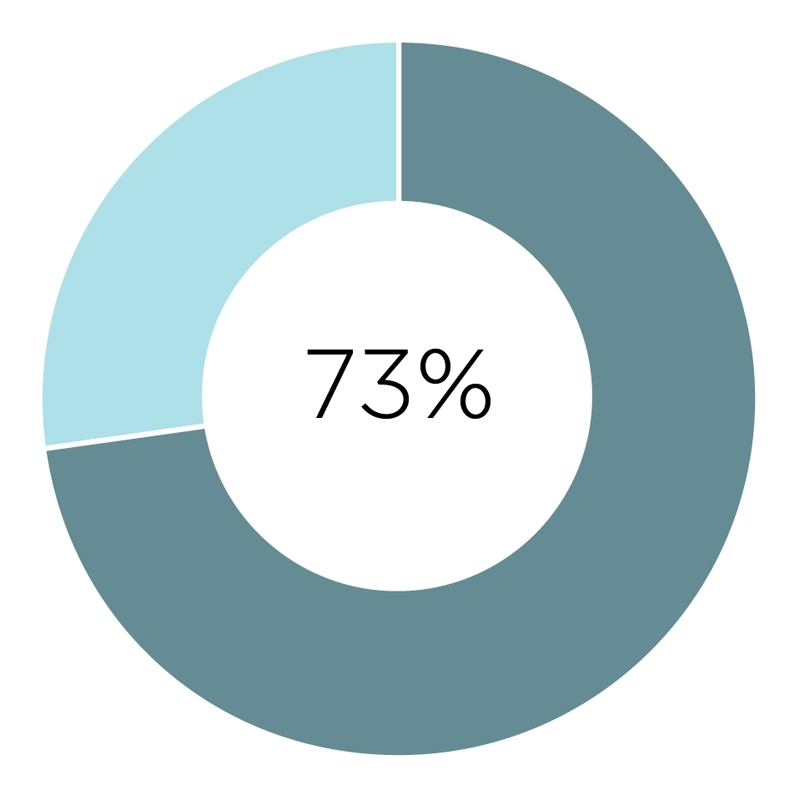

59% increased their credit score from their established starting point by a median of 77 points

74% established a credit score after being unestablished at intake

29% moved from a subprime score to a near-prime or prime score

Enrollment in helpful financial products

Enrollment in helpful financial products

66% took up at least one new financial product*

Better cash flow and savings

Better cash flow and savings

61% reduced their monthly debt payments by a median of $75*

56% increased their savings*

Growth in financial self-efficacy and power

Growth in financial self-efficacy and power

61% achieved at least one personalized financial goal*

48% increased their overall financial self-efficacy score**

*TrustPlus and Pathways clients only

**TrustPlus clients only; based on responses to a five-question survey regarding confidence in making financial decisions

Impact in Action

Data from our team of Financial Coaches in 2025 indicates that our approach is gaining traction and meaningfully impacting client trajectories out of debt. To measure progress out of debt, we use a framework with five indicators that signal greater financial security:

![]()

Reduced debt and predatory financial services

Lowering debt balances and using fewer high-cost, exploitative products

![]()

Healthy credit profiles

Achieving a near-prime or prime score

![]()

Access to helpful financial solutions

Being in a better position to be approved for safe, affordable financial products

![]()

Improved cash flow

Increasing cash flow, allowing for savings and investment in bigger financial goals

![]()

Increased financial self-efficacy and power*

Successfully meeting personal financial goals and feeling growing financial confidence and power that builds over time

*“How Executive Functioning and Financial Self-efficacy Predict Subjective Financial Well-Being via Positive Financial Behaviors,” Journal of Family and Economic Issues (2022)

2025 Impact Statistics

HERE’S HOW THESE INDICATORS SHOWED UP IN OUR 2025 CLIENT PORTFOLIO.

Reductions in debt and predatory financial services

Lower debt balances among clients with the following types of debt at intake

51% reduced personal loans by a median of $1,428

47% reduced credit card debt by a median of $1,345

65% reduced auto loan debt by a median of $4,228

58% reduced collections debt by a median of $1,068;

29% eliminated their collections entirely

63% reduced instances of predatory debt;

28% entirely eliminated predatory debt from their credit reports

Improvements to credit scores and profiles

59% increased their credit score from their established starting point by a median of 77 points

74% established a credit score after being unestablished at intake

29% moved from a subprime score to a near-prime or prime score

Enrollment in helpful financial products

66% took up at least one new financial product*

Better cash flow and savings

61% reduced their monthly debt payments by a median of $75*

56% increased their savings*

Growth in financial self-efficacy and power

61% achieved at least one personalized financial goal*

48% increased their overall financial self-efficacy score**

*TrustPlus and Pathways clients only

**TrustPlus clients only; based on responses to a five-question survey regarding confidence in making financial decisions

Reductions in debt and predatory financial services

Lower debt balances among clients with the following types of debt at intake

51% reduced personal loans by a median of $1,428

47% reduced credit card debt by a median of $1,345

65% reduced auto loan debt by a median of $4,228

58% reduced collections debt by a median of $1,068;

29% eliminated their collections entirely

63% reduced instances of predatory debt;

28% entirely eliminated predatory debt from their credit reports

Improvements to credit scores and profiles

59% increased their credit score from their established starting point by a median of 77 points

74% established a credit score after being unestablished at intake

29% moved from a subprime score to a near-prime or prime score

Enrollment in helpful financial products

66% took up at least one new financial product*

Better cash flow and savings

61% reduced their monthly debt payments by a median of $75*

56% increased their savings*

Growth in financial self-efficacy and power

61% achieved at least one personalized financial goal*

48% increased their overall financial self-efficacy score**

*TrustPlus and Pathways clients only

**TrustPlus clients only; based on responses to a five-question survey regarding confidence in making financial decisions

Products that Work for Workers

Not all financial products are created equal. At Neighborhood Trust, we define “good” or “safe” products as those that are affordable, accessible, and designed with the needs of underserved workers at their center—not products that exploit financial vulnerability for profit.

Good products are a critical connection point between people and the institutions that underpin the financial system. These products respond to the fact that traditional credit scoring and underwriting often fail to capture the full picture of a worker’s ability to manage their finances. They offer reasonable rates, transparent terms, and pathways to build, rather than damage, credit. Importantly, good products are offered by inclusive financial institutions (like CDFI credit unions) that provide a gateway to additional services that help workers grow their financial stability over time.

Neighborhood Trust has written extensively on the definition of predatory debt and its implications for consumers. While predatory products extract wealth and trap workers in cycles of debt, inclusive products—delivered through trusted institutions—help workers eliminate debt, build assets, and achieve lasting financial security.

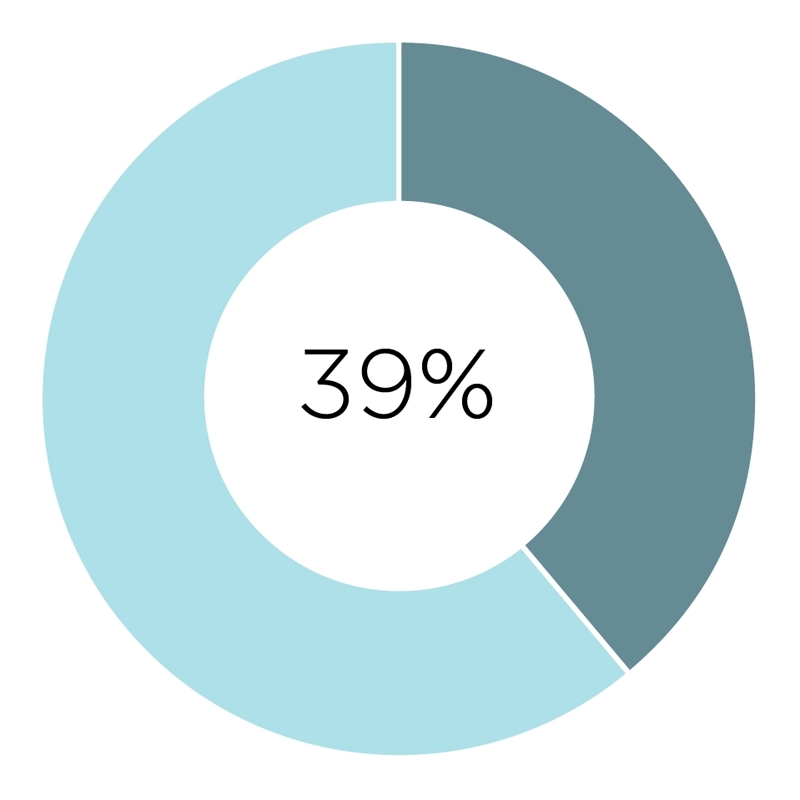

In 2025, Neighborhood Trust saw first-hand the financial impact of enrolling clients in safer financial products. Our clients with predatory debt are more likely to have subprime credit—67%, vs. 53% of those without any predatory debt—and low financial well-being scores—39% vs. 29%. This demonstrates both the damaging nature of these predatory products—as well as the ways those products create even more vulnerability to exploitation.

Products that Work for Workers

Not all financial products are created equal. At Neighborhood Trust, we define “good” or “safe” products as those that are affordable, accessible, and designed with the needs of underserved workers at their center—not products that exploit financial vulnerability for profit.

Good products are a critical connection point between people and the institutions that underpin the financial system. These products respond to the fact that traditional credit scoring and underwriting often fail to capture the full picture of a worker’s ability to manage their finances. They offer reasonable rates, transparent terms, and pathways to build, rather than damage, credit. Importantly, good products are offered by inclusive financial institutions (like CDFI credit unions) that provide a gateway to additional services that help workers grow their financial stability over time.

Neighborhood Trust has written extensively on the definition of predatory debt and its implications for consumers. While predatory products extract wealth and trap workers in cycles of debt, inclusive products—delivered through trusted institutions—help workers eliminate debt, build assets, and achieve lasting financial security.

In 2025, Neighborhood Trust saw first-hand the financial impact of enrolling clients in safer financial products. Our clients with predatory debt are more likely to have subprime credit—67%, vs. 53% of those without any predatory debt—and low financial well-being scores—39% vs. 29%. This demonstrates both the damaging nature of these predatory products—as well as the ways those products create even more vulnerability to exploitation.

Empowerment Over Exploitation:

SNAPSHOT OF SAFE FINANCIAL PRODUCT FEATURES

Fair Interest Rates

Fair products set APR to cover basic costs, not to exploit customers and maximize profits. Note that “reasonable” APR rates vary by product.

![]()

Transparent Fee Structure

Products should clearly communicate all fees, interest rates, and payment schedules to ensure clients understand the full cost and requirements before signing up.

Nuanced Underwriting

Decisions on who can access fair products go beyond credit score to consider cash flow, past repayment history on rent or utilities, social capital, and other qualitative data.

Customer Service

Products should come with reliable access to support so individuals can get questions answered, help with payments, and partnership to ensure the product is helping, not hurting, their financial goals.

Fair Interest Rates

Fair products set APR to cover basic costs, not to exploit customers and maximize profits. Note that “reasonable” APR rates vary by product.

![]()

Transparent Fee Structure

Products should clearly communicate all fees, interest rates, and payment schedules to ensure clients understand the full cost and requirements before signing up.

Nuanced Underwriting

Decisions on who can access fair products go beyond credit score to consider cash flow, past repayment history on rent or utilities, social capital, and other qualitative data.

Customer Service

Products should come with reliable access to support so individuals can get questions answered, help with payments, and partnership to ensure the product is helping, not hurting, their financial goals.

Safe Products in Action:

HOW THE FRESH START LOAN EQUIPPED WORKERS WITH OVER $1MILLION TO PAY OFF HIGH-INTEREST DEBT

![]() When workers are trapped in high-interest debt cycles, they need more than advice—they need better financial products. The Fresh Start Loan (FSL) is a zero-interest loan offered by Neighborhood Trust partner Hebrew Free Loan Society (HFLS) that helps individuals escape exploitative debt.

When workers are trapped in high-interest debt cycles, they need more than advice—they need better financial products. The Fresh Start Loan (FSL) is a zero-interest loan offered by Neighborhood Trust partner Hebrew Free Loan Society (HFLS) that helps individuals escape exploitative debt.

Neighborhood Trust regularly refers clients to HFLS, and in 2025 we helped expand the Fresh Start Loan beyond debt consolidation to address the full spectrum of financial pressures—from medical emergencies and legal fees to unexpected apartment repairs—based on needs our Financial Coaches were seeing. We also made FSL part of our newly launched Product Recommendation Engine, AI-powered technology which helps coaches more successfully and consistently identify eligible borrowers for products like the FSL.

In 2025, 66 Neighborhood Trust clients were approved for Fresh Start Loans, with an average loan amount of $15,848 and more than half (58%) receiving the maximum amount of $20,000. Last year, the FSL product put over $1 million in the pockets of workers who needed help to make ends meet.

The results* demonstrate the transformative power of connecting workers to inclusive products:

Credit card debt dropped dramatically from an average of $19,436 to $11,187, with 78% of clients reducing their debt by a median of nearly $8,000

Overall debt (including installment loans) decreased for 81% of participants, with a median reduction of over $13,209

Credit scores improved for 86% of clients, rising an average of 30 points

44% of participants moved up an entire credit tier—from Deep Subprime to Near Prime, Subprime to Near Prime, or Prime to Super Prime

The results* demonstrate the transformative power of connecting workers to inclusive products:

Credit card debt dropped dramatically from an average of $19,436 to $11,187, with 78% of clients reducing their debt by a median of nearly $8,000

Overall debt (including installment loans) decreased for 81% of participants, with a median reduction of over $13,209

Credit scores improved for 86% of clients, rising an average of 30 points

44% of participants moved up an entire credit tier—from Deep Subprime to Near Prime, Subprime to Near Prime, or Prime to Super Prime

*Results based on a sample of 36 clients tracked through follow-up credit reports

These are more than statistics. They represent workers who can now access mortgages, qualify for better auto loans, and escape the predatory debt trap that was costing them hundreds—sometimes thousands—of dollars annually in excess interest and fees.

“What’s unique about the Fresh Start Loan is that approval doesn’t require a 700+ credit score, which opens doors many banks keep closed. We’re flexible about past credit issues and focus on what’s happening now in terms of cash flow, repayment ability, and consistency.”

—Bernard Saavedra, Senior Financial Coach, Neighborhood Trust

“As a nonprofit, the Hebrew Free Loan Society designed this loan in response to borrowers’ financial realities. We incorporate a full-picture approach to help people reduce high-interest debt and make meaningful progress toward financial stability, not just keep up with monthly bills.”

—Eddie Ramos-Kleinman, Lending Partnerships Officer, HFLS

Safe Products in Action:

HOW THE FRESH START LOAN EQUIPPED WORKERS WITH OVER $1MILLION TO PAY OFF HIGH-INTEREST DEBT

![]() When workers are trapped in high-interest debt cycles, they need more than advice—they need better financial products. The Fresh Start Loan (FSL) is a zero-interest loan offered by Neighborhood Trust partner Hebrew Free Loan Society (HFLS) that helps individuals escape exploitative debt.

When workers are trapped in high-interest debt cycles, they need more than advice—they need better financial products. The Fresh Start Loan (FSL) is a zero-interest loan offered by Neighborhood Trust partner Hebrew Free Loan Society (HFLS) that helps individuals escape exploitative debt.

Neighborhood Trust regularly refers clients to HFLS, and in 2025 we helped expand the Fresh Start Loan beyond debt consolidation to address the full spectrum of financial pressures—from medical emergencies and legal fees to unexpected apartment repairs—based on needs our Financial Coaches were seeing. We also made FSL part of our newly launched Product Recommendation Engine, AI-powered technology which helps coaches more successfully and consistently identify eligible borrowers for products like the FSL.

In 2025, 66 Neighborhood Trust clients were approved for Fresh Start Loans, with an average loan amount of $15,848 and more than half (58%) receiving the maximum amount of $20,000. Last year, the FSL product put over $1 million in the pockets of workers who needed help to make ends meet.

The results* demonstrate the transformative power of connecting workers to inclusive products:

Credit card debt dropped dramatically from an average of $19,436 to $11,187, with 78% of clients reducing their debt by a median of nearly $8,000

Overall debt (including installment loans) decreased for 81% of participants, with a median reduction of over $13,209

Credit scores improved for 86% of clients, rising an average of 30 points

44% of participants moved up an entire credit tier—from Deep Subprime to Near Prime, Subprime to Near Prime, or Prime to Super Prime

*Results based on a sample of 36 clients tracked through follow-up credit reports

These are more than statistics. They represent workers who can now access mortgages, qualify for better auto loans, and escape the predatory debt trap that was costing them hundreds—sometimes thousands—of dollars annually in excess interest and fees.

“What’s unique about the Fresh Start Loan is that approval doesn’t require a 700+ credit score, which opens doors many banks keep closed. We’re flexible about past credit issues and focus on what’s happening now in terms of cash flow, repayment ability, and consistency.”

—Bernard Saavedra, Senior Financial Coach, Neighborhood Trust

“As a nonprofit, the Hebrew Free Loan Society designed this loan in response to borrowers’ financial realities. We incorporate a full-picture approach to help people reduce high-interest debt and make meaningful progress toward financial stability, not just keep up with monthly bills.”

—Eddie Ramos-Kleinman, Lending Partnerships Officer, HFLS

Guided by People, Enhanced by Technology

PUTTING AI TO WORK FOR SCALE AND IMPACT

Scaling a system of more inclusive financial services requires both innovation and human connection. Technology expands our reach, sharpens our insights, and improves our ability to recommend good financial products, while trusted guidance delivers the empathy and advocacy our clients need to improve their financial well-being.

At Neighborhood Trust, we are embracing continual advances in technology and AI. In 2025, we incorporated data and AI into our technology platform in safe, yet meaningful ways that set us up for ongoing innovation, efficiency, and scale.

HIGHLIGHTS FROM OUR WORK:

Solidified our Product Development team with the addition of David Bautista, our new VP of Product Management.

Launched our Financial Snapshot Tool, which applies the data from our clients’ financial profiles into a detailed, visual client financial dashboard. Clients and Financial Coaches can use the Snapshot Tool to quickly review scores, debt, savings, product enrollment, and short- and long-term financial goals.

Developed a prototype Product Recommendation Engine to dynamically recommend pre-vetted financial products for our clients, and built a proof-of-concept Credit Union Finder tool that helps clients find inclusive financial institutions nearby.

Developed a prototype Product Recommendation Engine to dynamically recommend pre-vetted financial products for our clients, and built a proof-of-concept Credit Union Finder tool that helps clients find inclusive financial institutions nearby.

Rolled out AI as a “copilot” for our Financial Coaches to handle administrative work, surface patterns, and capture session context so Coaches can focus on what technology cannot replicate: understanding the nuances of each client’s situation and navigating them through constantly shifting financial challenges.

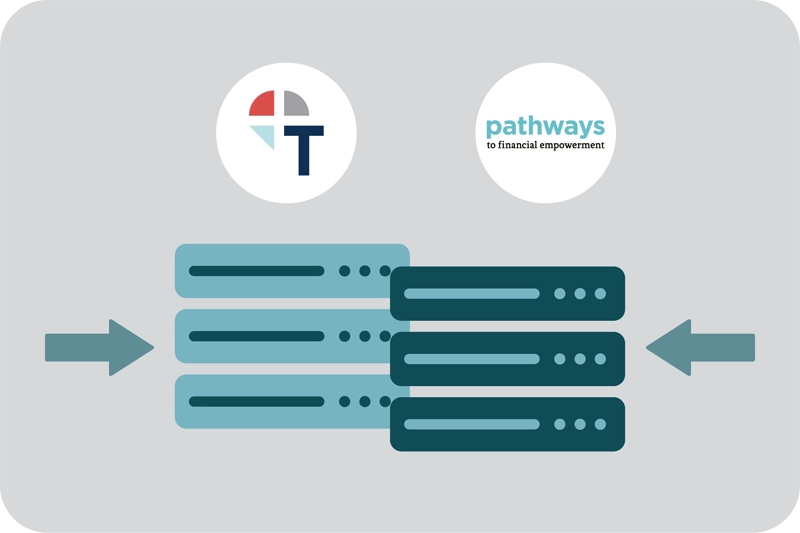

Made critical updates to our core data infrastructure and platform that will lay the groundwork for future AI development. We completed a significant project to merge the databases for our Pathways and TrustPlus programs, giving us a single, centralized data source to inform our large language model training, and ensuring that all innovative features can be released to our clients at once.

Made critical updates to our core data infrastructure and platform that will lay the groundwork for future AI development. We completed a significant project to merge the databases for our Pathways and TrustPlus programs, giving us a single, centralized data source to inform our large language model training, and ensuring that all innovative features can be released to our clients at once.

WHAT COMES NEXT

In 2026, we will build on these accomplishments by using AI to expand opportunities, access, and effectiveness across our entire client journey. We will evolve from a 1:1 financial coaching operation to offering a human+AI financial empowerment platform that triages clients into solution-specific paths based on their unique needs. A glance at what this will include:

A more robust, nationwide marketplace for responsible financial products: We will source cooperative financial products at scale by accessing and analyzing product eligibility and enrollment data from credit unions and CDFIs nationwide. This will help us serve more clients with more products, while also amplifying the reach of inclusive financial institutions by increasing their market visibility.

An effective, customized product-matching engine: We will develop an AI- and machine learning-powered product-matching engine that identifies the right product fit for a client based on their needs and profile. This engine will be layered beneath an intuitive user experience that uses intake data to automatically diagnose clients’ financial pain points, route them to the right financial solution, and provide a virtual financial coach to guide them as they select new, better products.

Smoother on-ramps to product enrollment: By connecting directly with partners’ systems through APIs, AI agents, and/or other channels, we will reduce or remove barriers to enrollment that can lead clients toward predatory alternatives.

“We are scaling technology to match our ambitions.”

—Theo Vaughn, Director of Product Services, Neighborhood Trust

![]() Listen to Theo talk about using technology to strengthen products and meet ever-evolving worker needs on Data-Driven Finance: The Financial Intelligence Podcast

Listen to Theo talk about using technology to strengthen products and meet ever-evolving worker needs on Data-Driven Finance: The Financial Intelligence Podcast

Institutions that Put Workers First

Neighborhood Trust is helping fuel a movement to strengthen and scale credit unions, which we believe represent the future of an equitable financial marketplace. CDFI credit unions and other mission-aligned financial institutions share a fundamental commitment: they measure success not by profit maximization, but by their ability to deliver financial security and mobility to the workers they serve.

A core part of Neighborhood Trust’s distribution model is embedding TrustPlus and Pathways as coaching services within partner credit unions. These complement existing credit union offerings by enhancing coaching services, improving digital tracking and measurement capabilities, enabling greater Coach-to-member communications, and expanding the program reach beyond what the credit union could do alone.

Shaped by a Legacy of Trust

OUR ROOTS AS A CREDIT UNION

Neighborhood Trust Financial Partners grew out of a financial coaching program within the Neighborhood Trust Federal Credit Union (NTFCU), a first-ever community development credit union established in Washington Heights in 1997. It was here that we first developed our model of delivering human-centered guidance, built specifically to meet the needs of the low-income New Yorkers who were walking through the doors of the credit union each day. NTFCU taught us the importance of trust as foundational to client service and set the bar for working with partners that put community first.

Today, Neighborhood Trust’s Financial Coaches maintain the spirit of the trusting relationships that make NTFCU and other credit unions across the country so special. And collaboration with credit unions and other mission-focused financial institutions will always be a part of our DNA.

Read more about our history and deep roots in the credit union movement.

Across the credit unions we served

Across the credit unions we served

4,898 credit union members received financial coaching

47 Financial Coaches were trained on our proprietary approach to financial coaching

The credit unions in our Pathways network are able to track their members’ outcomes in product enrollment. For the average credit union on our platform

The credit unions in our Pathways network are able to track their members’ outcomes in product enrollment. For the average credit union on our platform

46% of members who receive financial coaching open a credit and loan product

56% of members who receive financial coaching open an asset-building product with an average balance of $6,368

Across the credit unions we served

4,898 credit union members received financial coaching

47 Financial Coaches were trained on our proprietary approach to financial coaching

The credit unions in our Pathways network are able to track their members’ outcomes in product enrollment. For the average credit union on our platform

46% of members who receive financial coaching open a credit and loan product

56% of members who receive financial coaching open an asset-building product with an average balance of $6,368

“Too often, a loan decision ends with ‘no’ and no next step. Pathways was built to change that. We equip credit unions with Pathways so they can help members understand where they are, what’s holding them back, and how to move forward. So approval becomes possible, not just hoped for.”

—Hector Hidalgo, Account Manager, Neighborhood Trust

CDFI Credit Unions Are Central to Worker Financial Freedom

Credit unions prove that financial services can be delivered with both sustainability and purpose—demonstrating that serving individuals well and operating responsibly are not contradictory goals. By connecting workers to credit unions, we’re doing more than addressing an immediate debt problem; we’re building a financial system that works for workers, not against them.

These connections link workers to a broad range of inclusive products and services and long-term institutional partners invested in their financial well-being. Credit unions distinguish themselves as essential infrastructure for an equitable financial system through several key characteristics:

Gateway to opportunity, not just transactions. They offer pathways to comprehensive financial stability. A savings account opens doors to affordable mortgages, credit-building products, and financial counseling—positioning members for long-term success.

Affordability. Credit unions offer more competitive rates than large banks—often saving members thousands in fees and interest. For example, a typical consumer with a non-prime credit profile saves more than $8,000 over the life of a typical 72-month auto loan by financing at a credit union.

Community-responsive design. Rooted in specific communities, these institutions design products shaped by the needs they see firsthand. A credit union might offer on-site ITIN applications, affordable remittance options, or locally-tailored loan refinancing—responsiveness typically not found at large banks with standardized national products.

Meeting evolving financial needs. As individuals build stability, credit unions and CDFIs grow with them—from first savings accounts to auto loans, mortgages, or small business loans. This continuity means they don’t constantly rebuild trust as their financial lives evolve.

The cooperative advantage. Credit union deposits are reinvested directly in the community through loans to other members. Money circulates locally, enabling neighbors to support one another’s financial progress and strengthening the entire community’s capacity to access affordable credit.

Learn more about mission-driven CDFI credit unions as well as America’s 4,500 credit unions

Case Studies: Powering the Credit Union Movement

STORIES FROM THE FIELD

Neighborhood Trust x Border Federal Credit Union

Neighborhood Trust x Border Federal Credit Union

Del Rio, Texas

Border Federal Credit Union (Border FCU) serves 27,700 members along the U.S.-Mexico border, a predominantly Hispanic community where the average credit score hovers in the low 500s. Rather than turning away members with challenged credit, Border FCU designed several products—a Save & Score Visa card, a Credit Builder Loan and a Second Chance Auto Loan—all that require financial coaching from Pathways as a condition of approval.

By integrating Pathways coaching into the products, members have better financial outcomes, and coaches build stronger, more lasting relationships with members. Pathways data collection capabilities also help coaches adjust product features like interest rates on a case-by-case basis over time, as member credit improves.

“The ability to map each member’s journey changes everything. We can show members exactly where they started and where they’re headed. When they see their progress reflected in lower interest rates and better loan terms, they know we’re genuinely invested in their success. That’s why, even when life gets hard again, our members keep their commitment to us. They know we’ll find a way to help.”

—Monica, Financial Counselor, Border FCU

![]() Neighborhood Trust x Clearwater Credit Union

Neighborhood Trust x Clearwater Credit Union

Missoula, Montana

Clearwater Credit Union serves 65,000 members across 37 rural Montana counties where household incomes fall below the national average and financial emergencies can quickly destabilize families. Prior to partnering with Neighborhood Trust and implementing Pathways, Clearwater relied on paper files, a single certified financial counselor, and had no systemic way to track impact.

Pathways transformed Clearwater’s financial counseling services, expanding both the quality and reach. Operational impacts include:

Transitioned from paper files to a secure, streamlined digital system that ensures member confidentiality

Scaled counseling services across Montana’s rural geography through remote access—reaching members who previously couldn’t access in-person support

Supported team growth from one to four certified financial counselors, with Pathways training improving staff confidence and service standardization

Enabled real-time reporting that quantifies impact for counselors, credit union leadership and community stakeholders

Importantly, Pathways technology reinforces human connection rather than replacing it. Its text messaging platform helps counselors maintain trusted, ongoing touchpoints with members. As a result, members seek help proactively—before crises escalate—because support is accessible and counselors have the information they need to respond quickly and effectively.

![]()

“We tailor every experience because we listen closely week after week. We offer product recommendations members didn’t know existed, yet are capable of providing solutions. These interactions translate to joy. Members say, ‘You listened to me’ and this builds a connection that keeps them coming back. Making connections in this way is really a unique thing to do in financial services.”

—Sara Zeier, Director of Development Services, Clearwater Credit Union

Clearwater Member Impact (2017-2024):

Clearwater Member Impact (2017-2024):

1,177 clients served through Pathways

68% experienced credit score increases (average gain: 41 points)

53% established credit for the first time

$5m in non-real estate debt paid off

Case Studies: Powering the Credit Union Movement

STORIES FROM THE FIELD

Neighborhood Trust x Border Federal Credit Union

Del Rio, Texas

Border Federal Credit Union (Border FCU) serves 27,700 members along the U.S.-Mexico border, a predominantly Hispanic community where the average credit score hovers in the low 500s. Rather than turning away members with challenged credit, Border FCU designed several products—a Save & Score Visa card, a Credit Builder Loan and a Second Chance Auto Loan—all that require financial coaching from Pathways as a condition of approval.

By integrating Pathways coaching into the products, members have better financial outcomes, and coaches build stronger, more lasting relationships with members. Pathways data collection capabilities also help coaches adjust product features like interest rates on a case-by-case basis over time, as member credit improves.

“The ability to map each member’s journey changes everything. We can show members exactly where they started and where they’re headed. When they see their progress reflected in lower interest rates and better loan terms, they know we’re genuinely invested in their success. That’s why, even when life gets hard again, our members keep their commitment to us. They know we’ll find a way to help.”

—Monica, Financial Counselor, Border FCU

![]() Neighborhood Trust x Clearwater Credit Union

Neighborhood Trust x Clearwater Credit Union

Missoula, Montana

Clearwater Credit Union serves 65,000 members across 37 rural Montana counties where household incomes fall below the national average and financial emergencies can quickly destabilize families. Prior to partnering with Neighborhood Trust and implementing Pathways, Clearwater relied on paper files, a single certified financial counselor, and had no systemic way to track impact.

Pathways transformed Clearwater’s financial counseling services, expanding both the quality and reach. Operational impacts include:

Transitioned from paper files to a secure, streamlined digital system that ensures member confidentiality

Scaled counseling services across Montana’s rural geography through remote access—reaching members who previously couldn’t access in-person support

Supported team growth from one to four certified financial counselors, with Pathways training improving staff confidence and service standardization

Enabled real-time reporting that quantifies impact for counselors, credit union leadership and community stakeholders

Importantly, Pathways technology reinforces human connection rather than replacing it. Its text messaging platform helps counselors maintain trusted, ongoing touchpoints with members. As a result, members seek help proactively—before crises escalate—because support is accessible and counselors have the information they need to respond quickly and effectively.

![]()

“We tailor every experience because we listen closely week after week. We offer product recommendations members didn’t know existed, yet are capable of providing solutions. These interactions translate to joy. Members say, ‘You listened to me’ and this builds a connection that keeps them coming back. Making connections in this way is really a unique thing to do in financial services.”

—Sara Zeier, Director of Development Services, Clearwater Credit Union

Clearwater Member Impact (2017-2024):

1,177 clients served through Pathways

68% experienced credit score increases (average gain: 41 points)

53% established credit for the first time

$5m in non-real estate debt paid off

Scaling Impact through Collaboration

In 2025, in response to a significant weakening of the social safety net coupled with increased risks and financial strain on the most vulnerable individuals, Neighborhood Trust began building a coalition of nonprofit organizations whose staff and program participants could benefit from our financial coaching services.

We now work with three foundations that are making our financial coaching services available to their nonprofit grantees’ employees. This coalition is now 38 organizations strong, representing a reach of nearly 2,000 individuals across the country.

In addition to providing vital financial coaching services to individuals under financial stress, this coalition also aims to support the resilience of the social sector by helping to maintain our collective relevance to workers, reputations anchored in trust, and power to deliver our missions. In 2026 and beyond, we plan to continue expanding the coalition as part of our efforts to create as many connection points as possible between workers, mission-driven institutions, and safe financial products.

Conclusion

Throughout 2025, our bold vision of building a better financial products marketplace guided our efforts to reach 8,000+ workers with customized solutions and connections to community-driven financial institutions to help them progress toward freedom from debt.

In service of that commitment, we expanded the use of technology and AI to match workers with financial products that meet their needs, scaled our embedded financial coaching, and strengthened the systems that make safer, more accessible financial products possible. This work continues in 2026 and beyond, as we leverage AI to serve many multiples of today’s client base and amplify our impact across the financial landscape.

Learn more about us, and stay up-to-date on our latest initiatives. If you’re ready to shape a more equitable financial system, let’s start the conversation.

Follow Us